By Thomas Shapiro, David R. Pokross Professor of Law and Social Policy, and Director of the Institute on Assets and Social Policy

My academic and advocacy passions swirl around wealth inequality and how a lack of wealth drags families and communities down, a main ingredient of what I call "toxic inequality."

Rather than dwell on the ravages of deficit, the Institute on Assets and Social Policy and I partner with nonprofits, organizations and advocates to build solutions for better economic security for families and communities. That’s one reason emergency savings rises to the top tier of my policy wish list — an idea that’s taking root in philanthropies and think tanks, and even at the San Francisco airport.

For my book “Toxic Inequality,” my research team and I interviewed over 100 families in 1998-99 and again in 2010-11 about their finances, aspirations and prospects. Perhaps the results were not earth-shattering, but we were struck over and over again by how easily these hardworking families with sky-high ambitions for their children were thrown off-track by routine yet unplanned events like illness, a cutback in hours, loss of a job, the need to care for newborns or relatives, a broken-down car or a government shutdown.

It’s hard for working families in America today. Once our study subjects were thrown off-track, it often took them years to climb back to the same place, and those who did were lucky. Some even luckier ones had parents or other relatives who were able to help them weather a financial crisis; fewer still were able to move ahead on the wings of timely and considerable financial support. For too many, a single misfortune was too much to overcome: Plans came undone, and the family was never able to advance.

For me, these stories brought home the increasing financial precariousness of American families. And they are not alone. Indeed, the stories we heard are in many ways emblematic of how economics, race and wealth have congealed to historic levels of inequality, paralyzing Americans’ chances of getting ahead in these tough times.

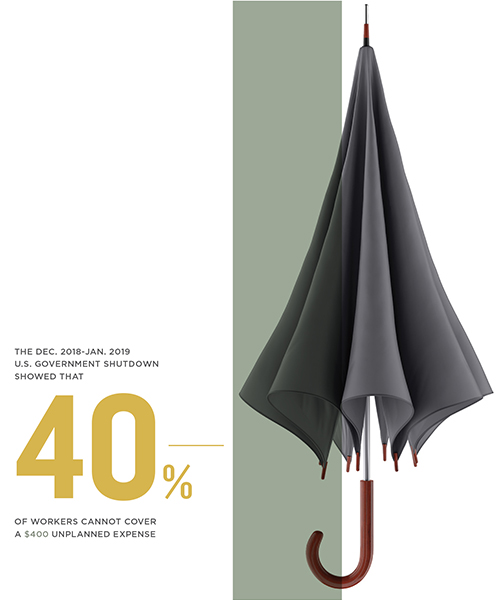

Four in 10 Americans cannot cover a $400 unplanned expense, and nearly two-thirds struggle to cover a $1,000 crisis. People go to the hospital. Cars break down. We know this from our studies. Low-income workers and families that rely on assistance programs tell us some months last longer than their paychecks. Yet it still is hard to fathom how this reality is becoming the story of mainstream America. Millions of American workers are a paycheck away from food pantries. The December 2018 - January 2019 government shutdown affecting 800,000 federal workers and 10,000 contractors brought that reality into the headlines, putting faces to the cold statistic that 40 percent of U.S. workers are unable to weather routine financial shocks.

People tend to plan for one mishap, if they can, but one adverse event often triggers a cascade of other stressful and traumatic events. I am ever-mindful of our conversations with Michelle and Kendrick Johnson (not their real names). When Kendrick lost his high-paying job, it unleashed economic, psychological, family and marital stresses from which he and Michelle could not recover. We don’t yet know how their daughter Desi dealt with these emotional and financial stresses and her parents’ ensuing separation. Now that Desi is in young adulthood, we also do not know how these stresses carried over to her family and career.

Workers who are paid a low wage are the most at risk. Let’s consider a family of three earning one paycheck equivalent to 125 percent of the federal poverty threshold, or about $24,000. Thirty percent of all workers, or 36 million people, fall into this category. Women, younger workers, Hispanic workers and those with some college are overrepresented among low-wage workers. Wages have stagnated the past 30 years and the largest job growth in the next decade is mostly in low-wage work with poor benefits. The future of work is trending in the wrong direction — toward more people working at jobs that pay low wages.

Policy offers no answers to meeting these unplanned expenses, other than accumulating lots of wealth or being born into a wealthy family. Since conducting those interviews, I (and many, many others!) have been trying to build an institutional rainy-day mechanism that would allow families to cover event-related financial hardships without unhinging all their hard work, plans and aspirations for their children.

One of the lessons we learned from the interviews involved the capacity of family wealth not only to navigate unplanned emergencies but to provide second, third, fourth, sometimes endless chances to “succeed.” We kept asking ourselves: Can we help innovate some institutionalized mechanism to serve similar functions as family wealth or inheritance to keep families from being thrown off-track so easily?

Emergency savings is one of the most promising and simple solutions to manage unexpected financial shocks. Money distresses us, especially low-wage workers close to the financial brink, where the need to meet bills too often results in taking predatory loans that typically make the situation worse. The emergency savings idea is quite simple: Employers provide a fund that workers can tap into in case of emergencies, say $1,000.

The idea is not preposterously optimistic. I am aware of several demonstration projects in the design phase or approaching a pilot phase. Organizations engaged in this work include the Workers Lab, the Rockefeller Foundation, BlackRock, the Center for Financial Services Innovation, Commonwealth, the Common Cents Lab at Duke University, and the City of San Francisco’s Office of Financial Empowerment and San Francisco International Airport.

Wait, the San Francisco airport??

Half of San Francisco airport’s 40,000 workers are paid less than $50,000. An emergency savings fund will help these workers cope with emergencies, stabilize their jobs, reduce reliance on predatory loans and ease the cycle of debt. The airport has committed resources and is listening to workers’ financial needs and concerns in order to design a rainy-day fund that would help boost their financial security. Over the past several months, I have come away from talks with several of the key players, and I am encouraged that pilot programs soon will be on the ground, perhaps with several designs to help us understand how to maximize impacts for workers and employment.

One option, a multi-stage design, particularly intrigues me because it melds economic security with workers’ power. In this model, contributions come from employers, so the fund is treated as a benefit. Workers can increase the fund with their own contributions, enabling them to exceed the $1,000 benefit ceiling and build in a borrowing facility to the workers’ fund. Such a workers’ fund would be controlled by workers and their representatives, and rules for distribution and decisions determined by a council of workers and employers.

This plan provides more security for workers and is good for employers, too. One in three workers say that financial stress is distracting at work. From a business point of view, that adds up to a lot of lost productivity each month. Distress over money and lower job satisfaction, in turn, leads to higher turnover and considerably higher hiring and training replacement costs.

It’s my privilege to work with and learn from advocates and groups across the country resisting the downward spiral of widening inequality and the violence of racial injustice. The need for emergency savings marks another profound failure manufactured by those who write the rules of the economy to benefit themselves at the expense of workers’ wages, benefits and income volatility. Absent these disturbing trends (and the knowledge that most new jobs in the next decade are expected to be just as bad), there would be little need for emergency savings programs.

Vehicles like emergency savings schemes fill in the downstream consequences and are an important redistribution palliative. My hope is for serious organizing, advocacy and policy action to generate a far more equitable distribution of the tremendous wealth we produce in the first place, thus drastically reducing crises for families.

The rules of the economy and politics are broken. Fortunately, the uncertainty and break-all-molds character of the current policy environment has also emboldened transformative ideas to enter the public square. Today’s is certainly a strange and dynamic policy environment, one that allows audacious ideas like emergency savings funds to take root. I am confident the Heller School will be an actor in these bold policy innovations. Stay tuned to see if they bear fruit.